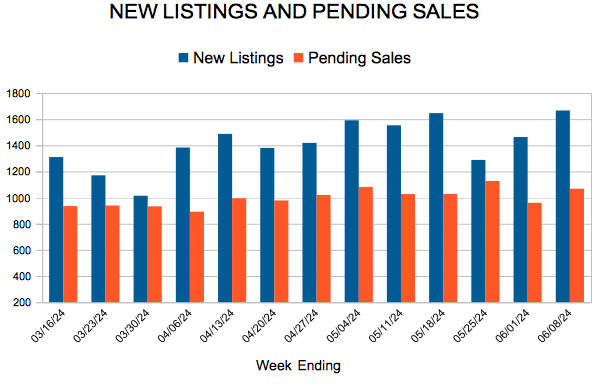

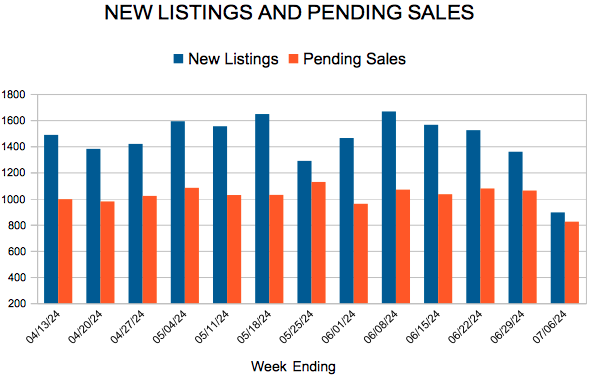

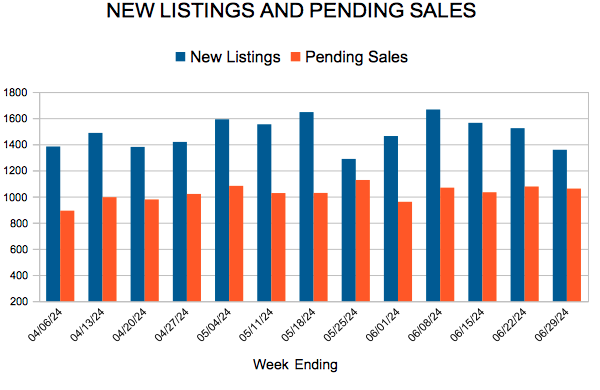

New Listings and Pending Sales

Growth in listings met by cooler demand leads to an increase in supply

(Jun. 18, 2024) – According to new data from Minneapolis Area REALTORS® and the Saint Paul Area Association of REALTORS®, listings rose slightly compared to last year while sales softened. Inventory levels and prices were up.

Sellers, Buyers and Housing Supply

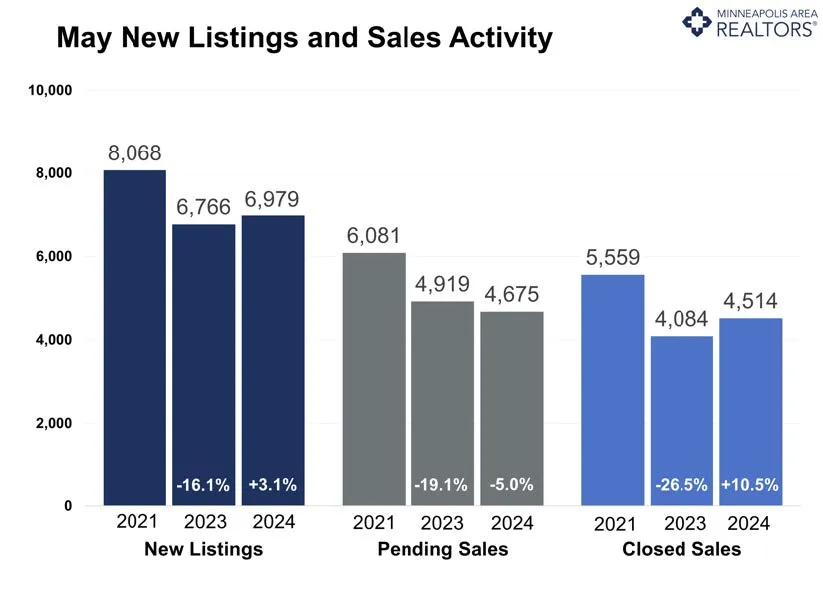

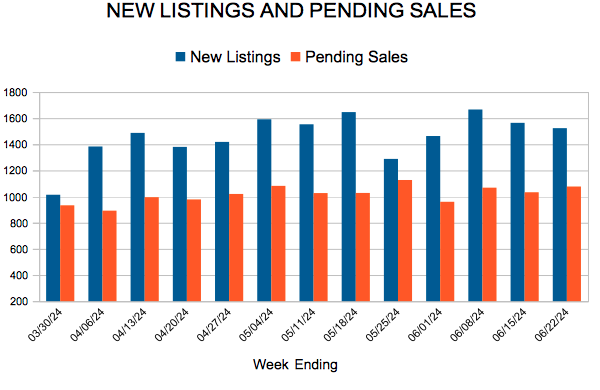

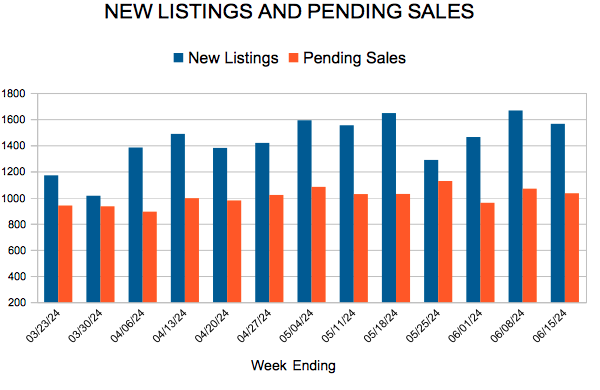

Buyers are starting to notice more inventory across the price spectrum. From under $200,00 to over $1,000,000, there are more homes for sale than there were a year ago. In fact, the number of homes for sale rose 15.7% from last year. That’s the highest number of active listings for May since 2020. And yet every price range—apart from $1,000,000 and above—remains a seller’s market where sellers are still getting strong offers relatively quickly. This year has seen growth in both listings and sales compared to 2023. For May, new listings are up 3.1% while sales fell 5.0%. One factor impacting May sales was higher than expected interest rates. Last May, rates were around 6.4% compared to 7.1% this year. Midyear is a good time to zoom out and look at some year-to-date figures. So far this year, seller activity is up 14.9% while buyer activity is up 5.3%.

A mix of stronger than expected economic data and continued inflation kept mortgage rates higher for longer and led financial markets to price in fewer rate cuts this year. But not everyone is feeling the benefits of the surprisingly resilient economy. Affordability remains a sticking point for would-be buyers—particularly first-time buyers without the equity from the last home to roll into the next. The typical monthly payment on the median-priced home is up over $1,000 since 2020.

There remains plenty of pent-up activity for both buyers and sellers. Even with the recent inventory gains, the market needs about 20,000 active listings to have a balanced market; currently there are fewer than 8,000. Buyers shopping the most affordable price points tend to be more rate-sensitive than luxury buyers who often use cash or have the financial wherewithal to simply absorb the higher payments. Some are able to skip the mortgage entirely by deploying cash. About 17.5% of Twin Cities homes are purchased in cash; it’s nearly double that for properties over $1 million.

Prices, Market Times and Negotiations

The median home price was up 4.1% to $385,000. Single family prices stood at $420,000, condo prices came in at $220,000 and townhomes checked in at $320,000. New home prices are just over $500,000 while existing home prices are $371,000. Even while they’re still in a relatively strong position, some sellers are finding themselves paying closing costs or incorporating other buyer incentives. “While the market is undergoing corrections, it is not a balanced market yet,” said Amy Peterson, President of the Saint Paul Area Association of REALTORS®. “Buyers need to remain both persistent and strategic ensuring their monthly payments align with their financial plans.”

Quality homes that show well in desirable areas are still getting multiple offers. Market-wide, sellers accepted offers at 100.1% of their list price, which was down from last year. Those purchase agreements were accepted after an average of 40 days on market, which was longer (slower) than last year. Every price point and area are unique. For example, single family homes are selling after 37 days but condos are taking 66 days. “While it’s true that each area and even market segment is unique, there are still some common threads,” said Jamar Hardy, President of Minneapolis Area REALTORS®. “Rising inventory is one of those themes, yet those shopping for homes shouldn’t assume we’re suddenly in a buyer’s market because we’re not.”

Location & Property Type

Since market activity always varies by area, price point and property type, housing markets shouldn’t be considered monolithic. Existing home sales performed better than new home sales. Single family sales fared better than condos or townhomes. Sales over $500,000 rose while sales under $500,000 softened. Cities such as Cambridge, New Richmond, Hugo and Buffalo saw among the largest sales gains while Arden Hills, Princeton, Medina and North Branch all had weaker demand. For cities with at least five sales, the highest priced areas were Wayzata, North Oaks, Excelsior and Mendota Heights. The most affordable areas were Norwood Young America, Albertville, Vadnais Heights and South St. Paul.

May 2024 Housing Takeaways (compared to a year ago)